#IkoKazi Code for Africa // Senior IoT Software Engineer

July 26, 2021

Pangea Blue Economy Accelerator Program // Apply before 29th August

July 29, 2021

Misperceptions about Venture Capital – A Problem By Stephen Muriithi

Venture Capital is funding provided to early growth companies i.e. startups at different stages of their growth evolution.

A Startup can be defined as an entity that experiences very rapid growth from the onset, and one that has the potential to scale quickly and generate huge returns for investors within a short period of time.

Paul Graham, Founder of YCombinator, indicates that most companies in a position to grow find that: –

- Taking outside money helps them grow faster.

- Their growth potential makes it easy to attract such money.

The Venture Capital Mindset:

It is extremely important that entrepreneurs take the time and effort to understand the mindset of a Venture Capitalist (VC). Gigi Levy-Weiss, a General Manager at NFX, a seed-stage venture firm based in San Francisco, has this hard truth to say, “For a startup, understanding a VC’s mindset is often as important as understanding the mindset of your customer. With no capital, most founders will not win, so you’d better learn the language.”

The Training Gap:

This is especially true in Africa. The Angel and Venture Capital industry are a fast-growing, but nascent industry across the continent, including South Africa, and we have not established any rigorous, robust training academies designed for entrepreneurs, founders, academics, policymakers, investors, or financiers on the technical mechanics of structuring a venture capital transaction.

Therefore, many Africans in Africa are at a distinct disadvantage when it comes to understanding the language of Venture Capital relative to their foreign counterparts. They may have relevant industry exposure via work experience, university seminars and training on entrepreneurship from academics, and/or have engaged in-person with real entrepreneurs who have bought and sold companies, who then guide them on what investors look for and how to prepare convincing pitches to venture investors. This is a classic case of ‘practice makes the master’ and perhaps may contribute towards assisting foreigners to secure an investment from global investors.

This access to exposure and technical training that foreigners based in Africa may have is a cold hard reality, that many Africans refuse to accept and face. With the exception of the Nigerian market, in my assessment, the default mechanism for most founders who fail to access early-stage funding is to resign to narratives of ‘discrimination.’

Partly, this is why I think there is a significant role for startup accelerators like Antler East Africa, YCombinator, and the Norrsken VC Impact Accelerator up in Rwanda that is actively trying to train aspiring African entrepreneurs on how to prepare viable, believable, investment case propositions for startup investment.

More on the impact of these startup accelerators in a separate post in the future. It is a first step in the right direction. However, it is not sufficient.

How Venture Capitalists Think:

The other side of the equation is understanding how VCs make money and their underlying mindset/mentality. To get a primer into VC economics, let’s start with some definitions.

The partners in a VC hold an entity called the General Partner (GP). Limited Partners (LPs) who are mostly institutional investors, bring in the money that GPs invest on their behalf. The GP only makes money once the LP’s initial investment is returned and they receive a return of approximately 20% of profits generated.

Case illustration:

If a Kshs. 100M fund, for example, returns only Kshs. 90M, the GP gets nothing. At Kshs. 300M, which is what great funds return (the “original” Kshs. 100M plus an additional Kshs. 200M of profit) the GP would get Kshs. 40M as their Carried Interest (this is for all the partners together combined).

This seems like a great return obviously. However, when we look at the holding percentages, early-stage VCs get diluted over time (shareholding reduces as more investors come on board, via funding rounds, and are issued with preferred stock) to approximately less than 10% by the time of an exit or liquidity event.

This means that to return a KES 300M fund, a fund would have to have invested in companies with an aggregate exit exceeding KES 3Bn! The chances of venture capital portfolio exits reaching such valuations are highly improbable especially in markets across Africa.

Therefore, VCs need really, really large exits. In addition, because the venture business is a hit-driven business the VCs need to get sufficient holding, usually 10-15% for a seed fund in any company to protect against the downside of all the companies that will fail.

These two aspects, the language of venture capital and the economics of how VCs make money, are scarcely understood across the continent, more so by first-time entrepreneurs. With a lack of knowledge, there is a lot of confusion about the type of companies venture capitalists fund.

The cardinal rule of financing according to Brad Feld; a co-founder of Techstars, an early-stage venture fund, and startup accelerator, is that everything starts and ends with market size as we have seen in the case illustration above.

“No matter how interesting or intellectually stimulating your business, if the ultimate size of the opportunity isn’t big enough to create a stand-alone self-sustaining business of sufficient scale, it may not be a candidate for venture financing.”

Industries of Interest:

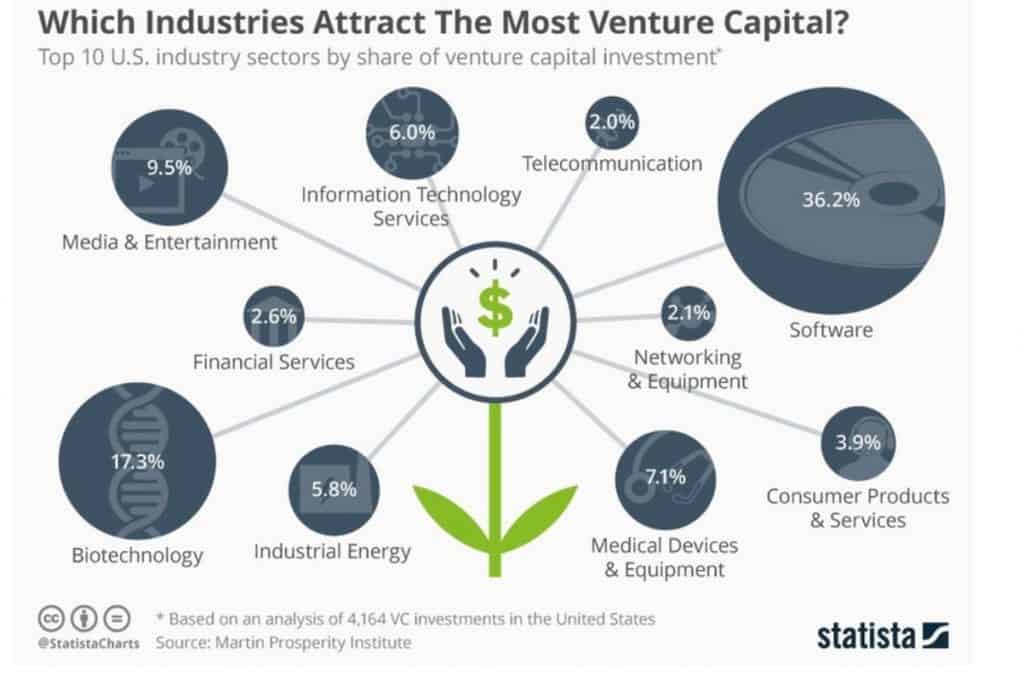

According to Statista, a German company specializing in market and consumer data, venture capital investment is heavily concentrated across several industrial sectors. As at 2015, the USA was leading the way with an estimated US $58.8 billion invested across the country. Statista notes that Software investment accounts for 36.2% of US VC funding, biotechnology at 17.3%, and Media and Entertainment accounting for 9.5% of total US venture capital investments as shown in the figure below.

Software companies get the largest share due to the onset of the Fourth Industrial Revolution and the fact that ‘software is eating the world’ as Marc Andreessen, a venture capitalist carefully articulated in a blog post in 2011.

Source: Statista 2016.

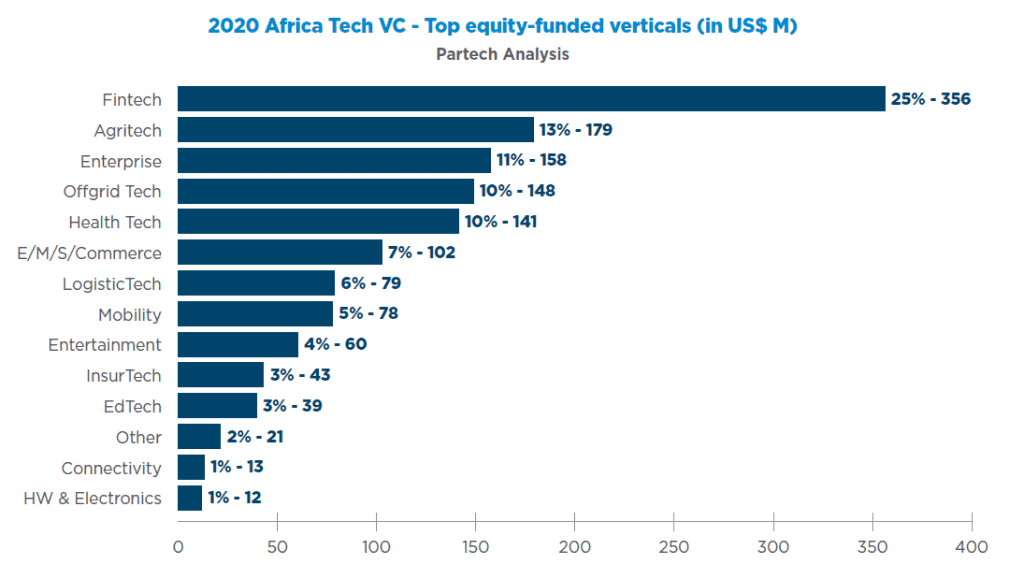

Contextualizing for Africa, the industry funding configuration looks rather different. Partech Partners, a global venture capital firm with offices in San Francisco, Paris, Berlin and Dakar issued the 2020 Africa Tech Venture Capital Report. In this report, Fintech, Agritech, Enterprise software, Offgrid Tech and Health Tech take the lion’s share of Africa funded investments as shown in the figure below.

Fintech accounts for 25% of total investments and is mainly concentrated in Nigeria (38%), Egypt (28%) and Ghana (13%). Agritech accounts for 13% with 79% of the equity funding concentrated in the Kenyan market according to the report. Enterprise accounting for 11% is concentrated in South Africa and is more aligned with the global patterns of funding as noted above.

Source: 2020 Africa Tech Venture Capital Report.

SMEs vs. Startups:

Many small-scale entrepreneurs who are not engaged in innovation-led businesses are unaware of these statistics and underlying sentiments of venture Capital investment and as a result, suffer frustration. A closer look at the funding coming into Africa is focused on a wide range of traditional and new industries that leverage technology to enhance their product/service offering.

To contextualize, if you have aspirations of opening up a pharmacy, a dental clinic, a Spa/Beauty parlour, a mitumba shop or a hardware store in Nairobi or Accra, you probably shouldn’t be approaching a venture capitalist for an investment.

- The potential for scalability (growth) is limited.

- The potential for outsized returns is restricted.

The more appropriate financial channels for such businesses would be to approach a micro-finance institution or a bank for working capital or business loans.

The Technology-Driven Imperative:

Innovation-driven businesses that often leverage technology (not exclusively e.g. hard tech/biotech) to scale and take advantage of a large market opportunity should have the ability to demonstrate to potential investors that the value of their investment can grow exponentially. This is a sentiment every entrepreneur must internalize.

Taking South Africa as an example, most South African-based VCs look to return to investors 10X their initial investment over a period of five years. This translates to a 50% y/y growth, according to Angelhub Ventures (a leading Angel group in South Africa that commenced operations in 2011) a growth projection that severely restricts the types of businesses VCs in South Africa would be keen to invest in.

In summary, there is an opportunity gap for well-structured, affordable training on the intricacies and nuances of venture capital and angel investing that is missing across the continent for all the stakeholders identified earlier.

The minute local investors and founders understand the risks and opportunities available in this industry, the higher the likelihood local capital access will be unlocked for local founders across the continent. Many rich local investors, who are mostly middle-aged, may not understand this business and will be unwilling to divert capital to investment propositions they do not fully understand or grasp.

In the next piece, we will look into some strategies that African markets can look into, to make local investor capital more available for innovation-driven technology businesses across Africa.

In the meantime, follow us on your LinkedIn pages:

About the Author:

Stephen Muriithi is the Founder of Brainhouse Capital. He is also a finance and strategy professional with extensive work experience working in the financial services industry for large multinational corporations in Kenya.

Stephen has over seven years working in the financial services industry having worked in the Vehicle and Asset Finance division as a Business Development Manager at Standard Bank Group, locally known as Stanbic Bank Kenya responsible for structuring finance facilities for major motor-vehicle and insurance dealerships across the country. Connect with Stephen here.

Brainhouse Capital

LinkedIn: https://www.linkedin.com/company/brainhouse-capital/?viewAsMember=true

Website: https://brainhousecapital.com/

{kind=link}

{kind=link}

{kind=link}